Income Tax Advantages

What makes 529 plans like New York's Advisor-Guided Plan such a popular way to save for college is the tax benefits they offer compared to traditional savings and investment accounts. Regardless of your income or tax bracket, you can take advantage of the federal and, if available, state tax incentives offered by these plans.

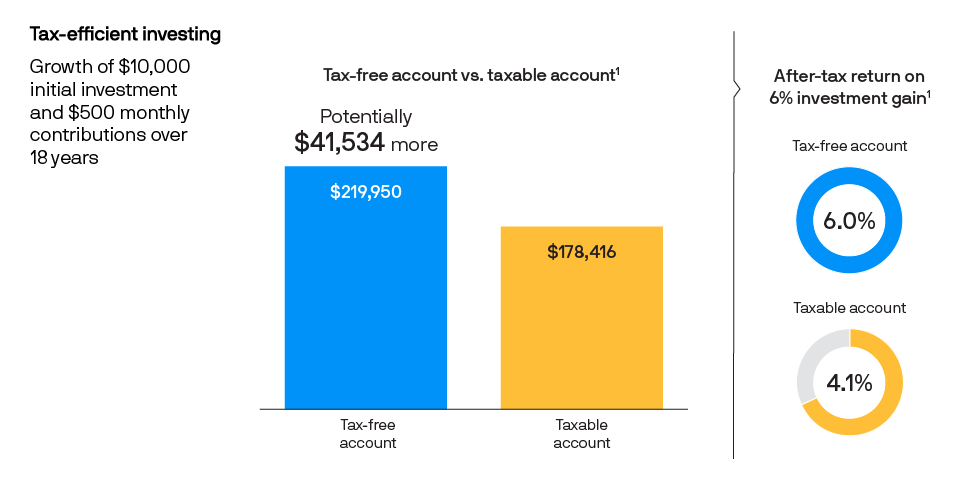

The power of tax-free growth

With the Advisor-Guided Plan, investment earnings compound on a tax-deferred basis, and qualified withdrawals are entirely free from federal and state income taxes.1 And because your account is tax-deferred, it has the potential to grow more quickly than taxable investments earning the exact same returns.

Accumulate $23,000 more with a tax-free 529 plan

Investment growth over 18 years

Source: J.P. Morgan Asset Management. Illustration assumes an initial $1,000 investment and monthly investments of $300 for 18 years. Chart also assumes an annual investment return of 6%, compounded monthly, and federal tax rate of 35%. Investment losses could affect the relative tax-deferred investing advantage. This hypothetical illustration is not indicative of any specific investment and does not reflect the impact of fees or expenses. Each investor should consider his or her current and anticipated investment horizon and income tax bracket when making an investment decision, as the illustration may not reflect these factors. These figures do not reflect any management fees or expenses that would be paid by a 529 plan participant. Such costs would lower performance. This chart is shown for illustrative purposes only. Past performance is no guarantee of future results.

Additional State Tax Benefits

In many states, residents or state tax payers get a full or partial state income tax deduction for investing in the state-sponsored 529 plan. In others, contributions to any 529 plan are eligible for the state's income tax deduction, and residents are not required to choose the in-state plan to get the benefit.

Learn more about the state tax benefits offered to New York State tax payers. Before investing, consider whether your or the beneficiary's home state offers any state tax or other benefits that are only available for investments in such state's qualified tuition program.

1 Earnings on non-qualified withdrawals may be subject to federal income tax and a 10% federal penalty tax, as well as state and local income taxes. New York State tax deductions may be subject to recapture in certain additional circumstances such as rollovers to another state's 529 plan and withdrawals used to pay elementary or secondary school tuition as described in the Disclosure Booklet and Tuition Savings Agreement. State tax benefits for non-resident New York taxpayers may vary. Tax and other benefits are contingent on meeting other requirements. Please consult your tax professional about your particular situation.

FAQs

Q. How do I open an Advisor-Guided Plan account?

A. You may open an account by contacting any broker or financial professional.

Need more information? Find answers to all your college savings questions here >