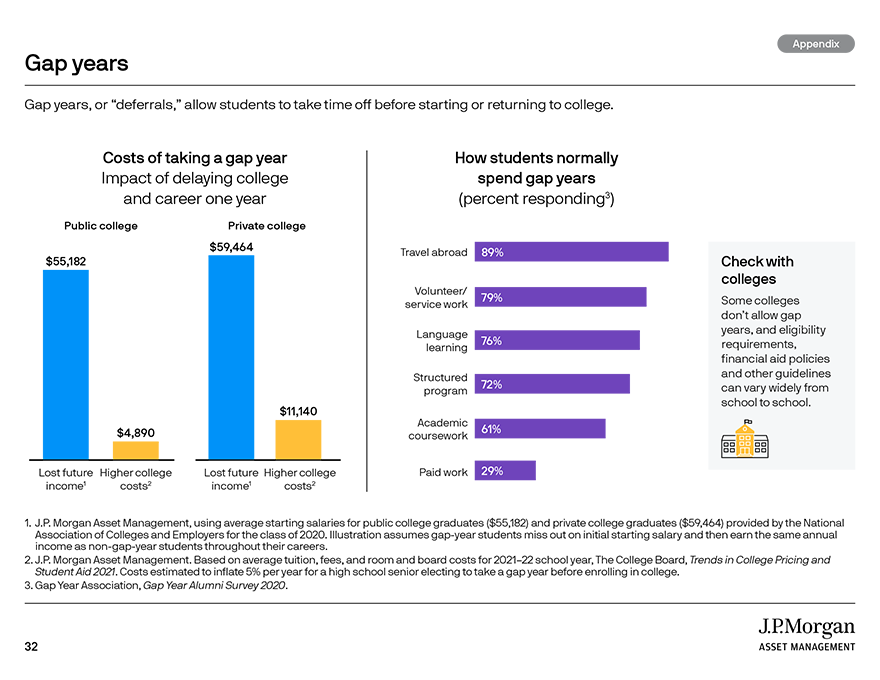

College is one of life’s most important ‒ and expensive ‒ investment goals. How much will it cost? What can you expect from financial aid? How can you invest and earn more while borrowing less?

View videos and select pages from College Planning Essentials to answer these questions and explore five time-tested strategies for successful investing. Together with guidance from your financial professional, it can help you make more informed decisions and the most of your college funds.

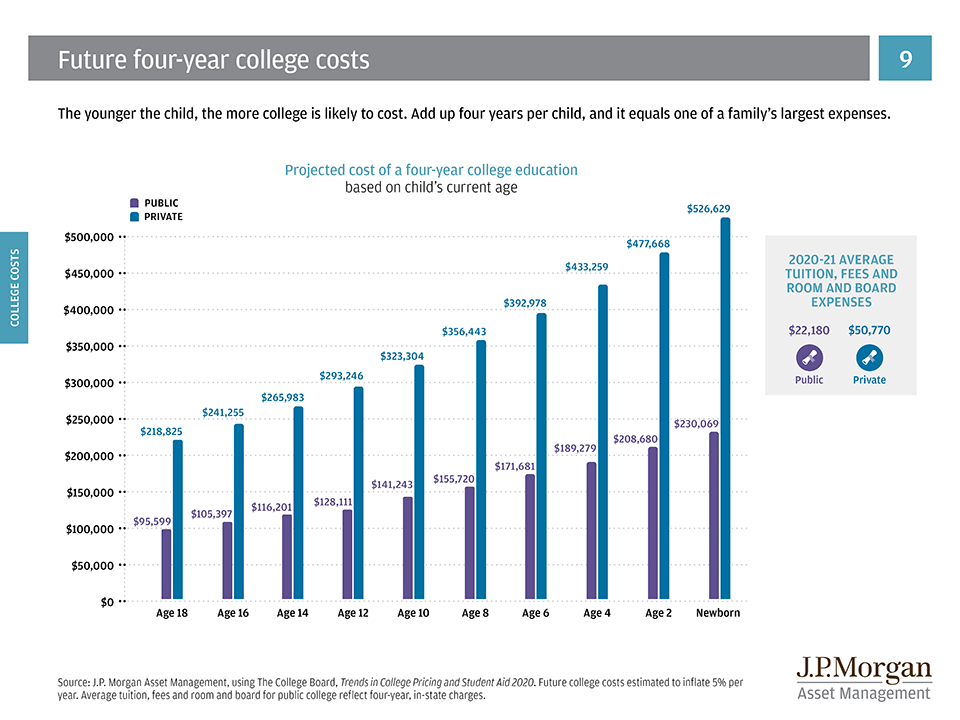

Understand the costs

See how much college could cost when a child is ready to enroll.

Start your plan with a college funding goal

The first step toward meeting college costs is knowing what they are. Costs are high today and will likely be even higher when your children attend college, thanks to annual tuition inflation that is outpacing the overall cost of living.1

Use this chart to estimate future costs and begin creating your investment plan. Simply find a child’s current age to see projected four-year costs at both public and private universities.

Next, work with your financial professional to determine how much you plan to pay and how much might come from financial aid, family gifts, student income and other funding sources.

EXAMPLE:

For a six-year-old, total costs are expected to be nearly $172,000 at a four-year public college and $393,000 for a private college.

1 J.P. Morgan Asset Management, College Planning Essentials 2021 Edition, Tuition inflation, page 8.

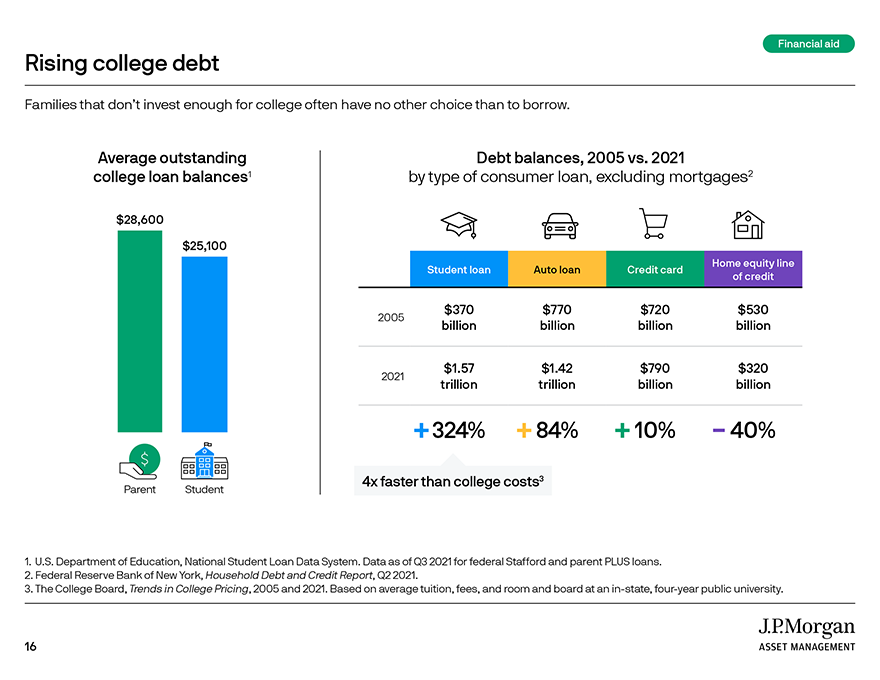

Know what to expect from financial aid

How much do grants and scholarships typically pay? Will investing hurt your financial aid eligibility? The answers may surprise you.

Free aid typically pays only a small part of college…and only if you qualify

Only about half of all students actually get grants and scholarships, and just 0.3% receive enough for a free ride to college.

Even if your child qualifies, grants pay an average of only 9% of the costs at a four-year public university, while scholarships cover just 12%.

To make up the difference, families need an investment plan that can help them achieve their goals without taking out expensive loans or ruling out schools based solely on cost.

Fewer students receiving free financial aid: Compared to the year before, 9% fewer students received grants and 7% fewer earned scholarships. That means higher out-of-pocket costs and a greater need to invest.

Don’t let financial aid stop you from investing

It’s a common myth that investing for college will hurt your chances for financial aid. The fact is, family income counts much more than assets in the formula for awarding federal aid.

This chart can help you estimate your Expected Family Contribution (EFC) used to determine federal financial aid eligibility. In calculating EFC, the Department of Education considers up to 47% of parents’ income but only a maximum of 5.64% of their assets ‒ even those in a 529 plan earmarked specifically for college.

HOW TO USE THIS CHART:

Find the box where your combined income intersects with the value of all assets except your primary home and retirement accounts. The result is your estimated Expected Family Contribution.

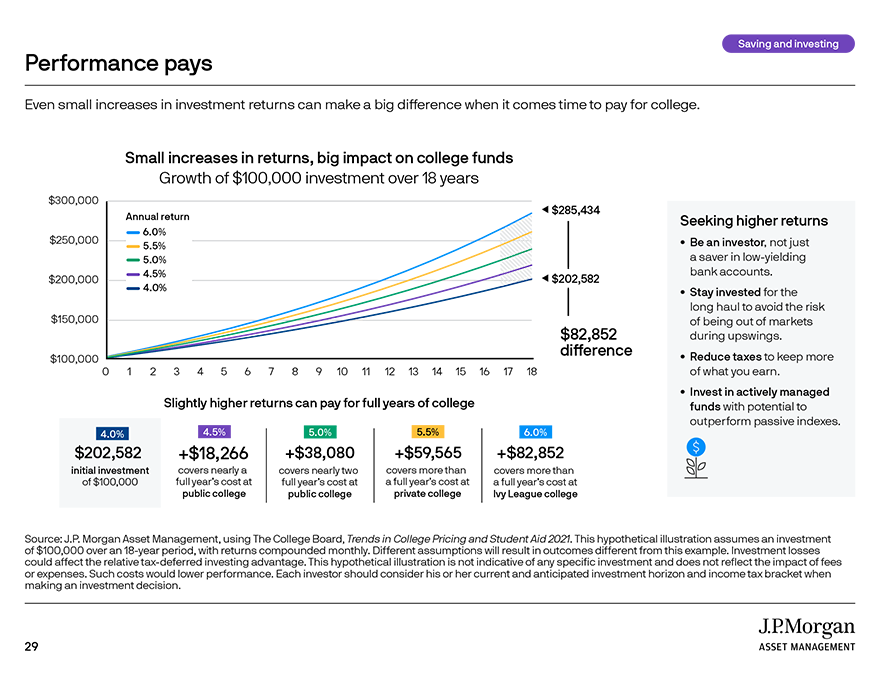

Don’t just save, invest

Savings alone won’t pay for college, but these investing tips can help you meet the costs.

Put the power of compounding to work for you

The sooner you start and the longer you invest, the more time your college fund may have to compound and grow in value.

For example, if you start contributing $500 a month when your child is born instead of waiting until age six, you would accumulate nearly $87,000 more. That’s the power of compounding.

Put your college investments on auto-pilot

Think of your college fund as another monthly bill and arrange for money to be automatically transferred from a bank account. You can supplement those monthly investments by also contributing part of pay raises, bonuses, tax refunds and other extra cash. Every small addition could make a big difference over time.

Don’t count on cash

The most commonly used college funding vehicles are savings accounts, checking accounts and CDs that have normally underperformed tuition inflation.1 Instead of just saving, investing that cash gives families the higher return potential needed to grow college funds and keep pace with rising costs.

Invest in a diversified portfolio

The key to staying invested for the long term is avoiding large portfolio fluctuations over the short term. Because stocks and bonds tend to rise and fall at different times, owning both may help you smooth out investment returns and stay on course toward college funding goals.

This chart shows that a diversified portfolio has historically outpaced bond returns and tuition inflation, with lower volatility than stocks.

1 ISS Market Intelligence, 529 Industry Analysis 2020.

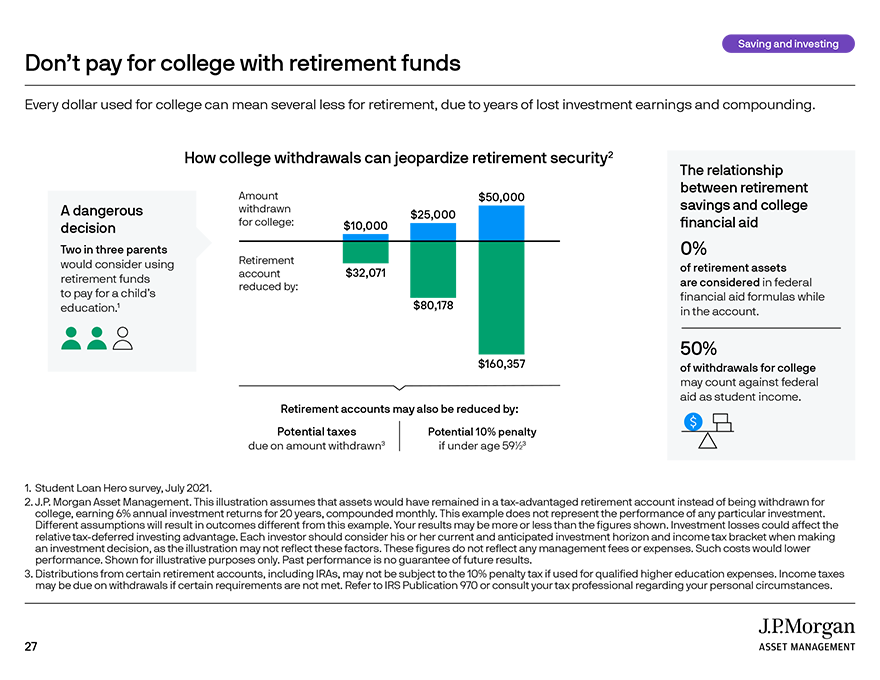

Keep college and retirement accounts separate

Discover how every retirement dollar spent on college can mean several less for life after work.

Avoid using retirement funds for college

Withdrawing money for college can jeopardize your retirement security. For example, this chart shows that taking $25,000 to fund college now could mean $80,000 less for retirement in 20 years, due to lost investment earnings and compounding.

Spending retirement money on college may also result in taxes, penalties and reduced financial aid. Because withdrawals are considered student income, half of the amount you take may count against your federal aid package.

Consider opening dedicated accounts just for college, such as 529 plans, which offer special tax benefits not available in retirement accounts.

Make the most of tax-advantaged 529 plans

A 529 plan offers valuable tax benefits not available in other college accounts. See how they can help you reduce taxes and increase estates.

Keep more of what your investments earn

Taxes can erode investment returns and leave families with less for college. With a 529 plan, investment earnings and withdrawals are completely tax free when used to pay qualified education expenses.1

The result: In our example from the video above, the 529 plan is worth nearly $48,000 more than a taxable investment receiving the same contributions and earning the same returns.

In addition, many states allow investors to deduct 529 plan contributions from state income, enabling them to save even more on taxes.

Maximize special gift and estate tax benefits

529 plans allow five years of tax-free gifts in a single year – up to $75,000 per child from individuals and $150,000 from married couples.2

One lump-sum gift at birth may be enough to pay most of the total projected four-year public and private college costs, as shown in the chart.

All 529 plan gifts and investment earnings are removed from the contributor’s estate without losing control over the assets. This can help grandparents, aunts, uncles and others invest for college while also reducing estate taxes, increasing inheritances and creating family legacies.

1 Earnings on federal non-qualified withdrawals may be subject to federal income tax and a 10% federal penalty tax, as well as state and local income taxes. New York State tax deductions may be subject to recapture in certain additional circumstances such as rollovers to another state’s 529 plan, or withdrawals used to pay elementary or secondary school tuition (“K-12 Tuition Expenses”), registered apprenticeship program expenses (“Apprenticeship Program Expenses”), or qualified education loan repayments (“Qualified Education Loan Expenses”) as described in the Disclosure Booklet and Tuition Savings Agreement. State tax benefits for non-resident New York taxpayers may vary. Tax and other benefits are contingent on meeting other requirements. Please consult your tax professional about your particular situation.

2 No additional gifts can be made to the same beneficiary over a five-year period. If the donor does not survive the five years, a portion of the gift is returned to the taxable estate.